RBI Cyber Security Framework: Complete Compliance Guide for Banks (2026)

Last Updated date: July 12, 2026

On this page

See Tech Prescient in Action

Automate access, reduce risk, and stay audit-ready

The Reserve Bank of India (RBI) is the central banking authority responsible for regulating India's monetary policy and overseeing the stability of the banking system. As financial services have rapidly digitized, the RBI has expanded its role beyond traditional regulation to actively address cybersecurity risks across the sector.

With a growing share of banking transactions now happening online and through mobile platforms, the attack surface for financial institutions has increased significantly. At the same time, rising incidents of data breaches and cyber threats have made it clear that a consistent, sector-wide approach to cybersecurity is no longer optional, it is essential.

This is where the Reserve Bank of India (RBI) Cyber Security Framework comes into play. Introduced in 2016, it mandates a structured, risk-based approach for banks to protect systems, detect threats, and respond to incidents while ensuring accountability at the board level. As digital banking continues to expand, the framework plays a critical role in safeguarding customer data and maintaining trust in the financial ecosystem.

Let's explore the framework in detail and understand what it takes to stay compliant and secure.

Key Takeaways:

- The Reserve Bank of India Cyber Security Framework mandates a risk-based security approach for banks

- Banks must implement 24/7 C-SOC monitoring and perform regular VAPT testing

- The framework requires strict incident reporting and a Cyber Crisis Management Plan

- An RBI compliance checklist ensures governance, security controls, and risk coverage

- M1 to M4 levels define cyber maturity, along with key gaps and governance needs

What Is the RBI Cyber Security Framework?

The Reserve Bank of India Cyber Security Framework is a regulatory mandate introduced in 2016 that requires scheduled commercial banks to adopt a structured, risk-based approach to cybersecurity. It establishes cybersecurity as a board-level responsibility and ensures that institutions implement strong mechanisms for prevention, detection, and incident response.

While the framework was initially designed for commercial banks, its scope has expanded over time to include cooperative banks and payment system operators (PSOs). This broader applicability reflects the need to secure the entire financial ecosystem as cyber threats become more advanced and interconnected.

The framework focuses on protecting financial infrastructure and customer data through continuous monitoring, well-defined security controls, and mandatory incident reporting practices.

At a high level, the framework is built around three core pillars:

1. Baseline Cyber Security and Resilience Requirements

This pillar defines the minimum security controls banks must implement to maintain a strong security posture. It covers areas such as user access control, patch management, data leak prevention, vendor risk management, and employee awareness programs.

It also emphasizes maintaining a comprehensive, up-to-date inventory of IT assets including hardware, software, and critical data flows, along with ensuring the protection of customer data both at rest and in transit. These controls form the foundation of cybersecurity across systems and operations.

2. Cyber Security Operations Center (C-SOC)

Banks are required to establish a dedicated Cyber Security Operations Center to enable continuous, 24/7 monitoring of their IT environment. The C-SOC is responsible for threat detection, log management, incident analysis, and integration with SIEM tools, supported by skilled personnel and defined processes.

It also leverages advanced detection techniques, including tools such as honeypots, to identify both known and emerging attack patterns more effectively.

3. Cyber Security Incident Reporting (CSIR)

The framework mandates timely reporting of cybersecurity incidents to the Reserve Bank of India through the CSITE cell. Banks are required to report all unusual, successful, or attempted cyber incidents within 6 hours of detection, ensuring rapid regulatory visibility.

They must also share root cause analysis and continue providing updates until resolution, enabling transparency and effective oversight.

Why Did RBI Introduce the Cyber Security Framework?

The Reserve Bank of India introduced the Cyber Security Framework to address the rapid rise in digital banking, increasing cyber fraud, and growing systemic risks within the financial sector. As banks expanded their digital services, the threat landscape evolved just as quickly, making it essential to establish a unified, enforceable approach to cybersecurity. The framework ensures that banks move beyond reactive security and adopt a proactive, risk-based model that safeguards financial systems and customer data.

The need for the framework is driven by several key factors:

1. Growth of Digital Payments

The surge in online and mobile banking has significantly expanded the attack surface for financial institutions. With more transactions happening digitally, banks must secure systems, networks, and endpoints against evolving threats.

2. Increasing Cyber Fraud

Banks are prime targets for cybercriminals, making fraud detection and prevention a critical priority. The framework enforces mechanisms like continuous monitoring, VAPT, and incident response to reduce the risk of breaches and financial loss.

3. Regulatory Push for Resilience

RBI has strengthened compliance expectations by introducing structured requirements such as board-approved policies, independent compliance functions, and risk-based internal audits. Roles like the Chief Compliance Officer (CCO) and practices like compliance testing ensure accountability and governance.

4. Protection of Customer Financial Data

With sensitive financial data at stake, the framework emphasizes data protection across its lifecycle. Controls such as access management, data leak prevention, and vendor risk management help banks maintain confidentiality, integrity, and trust.

Quick Check

Can your bank detect and report an incident within 2–6 hours? If not, your response readiness may already be a compliance gap.

Key Components of RBI Cyber Security Framework

The RBI Cyber Security Framework is built on governance, baseline security controls, continuous monitoring via C-SOC, periodic VAPT testing, and strict incident response mechanisms. It ensures that banks can identify risks, protect critical assets, detect threats in real time, and respond effectively while maintaining regulatory compliance.

Governance & Board-Approved Policy

Cybersecurity is driven at the board and senior management level, making it a core business responsibility. Banks must define a clear cyber risk appetite and establish a board-approved cybersecurity policy aligned with business and regulatory requirements. This includes clearly defined roles and accountability across teams, along with continuous risk assessment practices. Regular reviews and audits ensure that policies remain effective against evolving cyber threats.

Baseline Security Controls

The framework mandates essential controls to maintain a minimum level of cyber resilience across systems. Banks must enforce strong access control and identity management, implement timely patch management, and deploy data leak prevention mechanisms to secure sensitive data. It also requires network segmentation to isolate critical systems, along with maintaining an up-to-date IT asset inventory. Employee awareness and training programs further strengthen the human layer of security.

Cyber Security Operations Center (C-SOC)

Banks are required to establish a 24/7 Cyber Security Operations Center to ensure continuous monitoring of their IT environment. The C-SOC enables real-time threat detection through log management, event correlation, and integration with SIEM tools. It plays a critical role in identifying suspicious activities early and supporting timely incident response.

Pro Tip

Don't treat SOC as just monitoring. Integrate identity with SIEM to catch privilege misuse in real time.

VAPT Requirements

The framework emphasizes periodic Vulnerability Assessment and Penetration Testing to evaluate the effectiveness of security controls. Banks must conduct regular vulnerability assessments and annual penetration testing, often validated by third-party experts. These exercises help identify weaknesses, validate defenses, and ensure systems are resilient against real-world attack scenarios.

Incident Response & Reporting

Banks must implement a structured incident response mechanism supported by a Cyber Crisis Management Plan (CCMP). The framework mandates reporting of cybersecurity incidents to RBI through the CSITE cell within defined timelines, typically within 2 to 6 hours of detection. Institutions are also expected to provide root cause analysis and updates until the incident is fully resolved.

Third-Party & Vendor Risk Management

The framework requires banks to manage risks arising from third-party vendors and service providers. This includes conducting due diligence before onboarding, defining security clauses in contracts, and continuously monitoring vendor activities. Ongoing assessments ensure that external dependencies do not introduce vulnerabilities into the banking ecosystem.

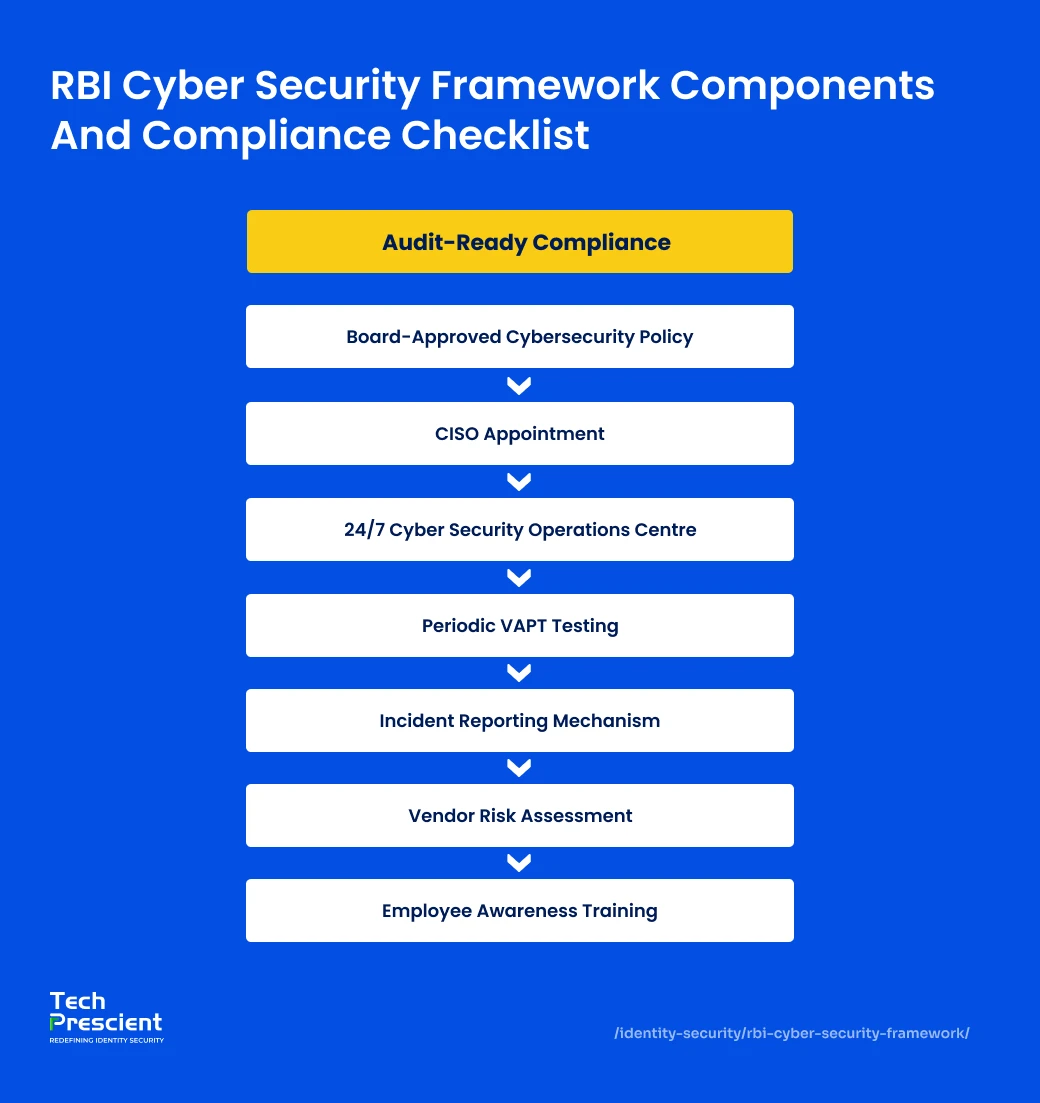

RBI Cyber Security Framework Checklist for Banks

Banks must follow a structured compliance checklist including governance policies, SOC monitoring, VAPT testing, incident reporting, and vendor risk management to meet RBI requirements. The framework requires institutions to not only implement security measures but also validate, review, and improve them on an ongoing basis to maintain a strong cybersecurity posture.

Here's a practical RBI cyber security framework checklist for banks:

1. Board-approved cybersecurity policy

Banks must establish a formal, board-approved cybersecurity policy that clearly defines their security strategy, risk appetite, and governance structure. This policy should be reviewed at least annually and supported by proper documentation to demonstrate compliance during audits.

2. CISO appointment

A qualified Chief Information Security Officer (CISO) must be नियुक्त to lead the cybersecurity function, ensure enforcement of policies, oversee risk management practices, and report directly to senior management or the board to maintain independence and accountability.

3. Operational 24/7 SOC

Banks are required to maintain a fully operational Cyber Security Operations Center (C-SOC) that continuously monitors systems, analyzes logs, detects anomalies, and enables real-time response to potential threats using tools like SIEM and threat intelligence.

4. Periodic VAPT

Regular Vulnerability Assessment and Penetration Testing (VAPT) must be conducted to identify security weaknesses. These assessments should be risk-based, performed periodically, and validated by independent third parties to ensure effectiveness of controls.

5. Incident reporting mechanism

A well-defined incident response framework must be in place, including a Cyber Crisis Management Plan. Banks must report cybersecurity incidents to RBI's CSITE within stipulated timelines, along with detailed analysis and remediation updates.

6. Vendor risk assessment

Banks must carry out thorough due diligence before onboarding vendors, include security and audit clauses in contracts, and continuously monitor third-party risks to ensure they do not introduce vulnerabilities into the ecosystem.

7. Employee awareness training

Regular cybersecurity awareness and training programs must be conducted across all levels of the organization to educate employees on threats such as phishing, social engineering, and safe security practices.

This checklist ensures that banks maintain strong governance, continuously assess risks, validate their defenses, and remain fully aligned with RBI's cybersecurity compliance requirements.

Want a complete, audit-ready version of this checklist?

Download a structured RBI compliance checklist to validate controls, track gaps, and prepare for audits with confidence.

What Are M1, M2, M3, M4 Levels by RBI?

The Reserve Bank of India categorizes the total money supply in the Indian economy into four levels, M1, M2, M3, and M4, based on liquidity, or how easily assets can be converted into cash, and their underlying components. These classifications help the RBI assess liquidity conditions, manage inflation, and guide monetary policy decisions.

In simple terms, as you move from M1 to M4, cybersecurity maturity evolves from basic controls to proactive, intelligence-driven security.

M1: Basic Compliance

M1 is the most liquid category of money supply, comprising funds that are readily available for immediate use in transactions. It includes currency held by the public, demand deposits with the banking system, and other deposits with the Reserve Bank of India, where demand deposits refer to balances in current and savings accounts that can be withdrawn at any time.

M2: Structured Controls (intermediate measure)

M2 is a slightly broader measure than M1, while still classified as narrow money, as it includes M1 along with savings deposits held in post office savings accounts. Its components consist of M1 plus savings deposits with Post Office Savings Banks.

M3: Advanced Monitoring (broad money)

M3 is the most widely used indicator of the total money supply in the economy. Referred to as broad money, it includes not only liquid funds but also time deposits that are not immediately accessible. Its components consist of M1 along with time deposits such as fixed and recurring deposits held with the banking system. The Reserve Bank of India primarily relies on M3 for monetary policy decisions and inflation management.

M4: Proactive Intelligence-Driven Security (broadest measure)

M4 represents the broadest measure of money supply, capturing the total monetary resources in the economy. It includes M3 along with all deposits held in post office savings institutions, excluding instruments such as National Savings Certificates.

Who Must Comply with RBI Cyber Security Framework?

The RBI Cyber Security Framework applies primarily to banks and extends to NBFCs, payment institutions, and other regulated financial entities handling critical financial data. The goal is to ensure that all institutions operating within India's financial ecosystem follow a consistent and robust approach to cybersecurity and risk management.

Institutions required to align with the framework include:

1. Scheduled Commercial Banks

Public and private sector banks that form the backbone of India's banking system are the primary entities governed by the framework.

2. Foreign Banks in India

Branches and subsidiaries of international banks operating within India must comply with RBI cybersecurity expectations.

3. Cooperative Banks and Regional Rural Banks (RRBs)

Both urban and rural cooperative institutions, along with RRBs, are expected to implement similar cybersecurity controls to safeguard local banking operations.

4. Non-Banking Financial Companies (NBFCs)

NBFCs are brought under the framework through extended IT governance and outsourcing guidelines, ensuring they maintain strong cyber resilience.

5. Payment Banks and Small Finance Banks

These specialized institutions, focused on financial inclusion and digital services, must adopt secure practices to protect high-volume transactional environments.

6. Payment System Operators

Entities managing payment and settlement systems are required to follow strict cybersecurity and reporting norms due to their critical role in financial infrastructure.

In addition to entity coverage, the framework applies across all critical operational areas within these institutions. This includes IT infrastructure, core banking systems, digital banking channels, cloud environments, data centers, ATM networks, POS systems, internal employee systems, and third-party service providers.

To strengthen incident response and national-level coordination, institutions are also expected to align with reporting practices involving the Indian Computer Emergency Response Team, ensuring timely escalation and response to cybersecurity incidents.

By extending its scope across institutions and operational layers, RBI ensures that cybersecurity is consistently enforced across every potential entry point in the banking ecosystem.

Common Compliance Gaps Banks Face

Banks often face compliance gaps due to weak identity controls, delayed incident reporting, lack of centralized monitoring, and poor third-party risk management. These gaps often emerge not because controls are absent, but because they are not properly enforced, monitored, or documented across systems and processes.

Here are the most common compliance gaps observed across banks:

Over-permissioned user accounts

Excessive access rights remain one of the biggest risks, where users retain privileges beyond their roles. This violates least privilege principles and increases the chances of misuse or unauthorized access.

Weak identity lifecycle management

Many institutions lack strong processes for provisioning, reviewing, and deprovisioning user access. Without proper identity governance, dormant accounts and role mismatches create hidden security vulnerabilities.

Delayed incident reporting

RBI mandates strict timelines for reporting incidents to CSITE, but delays often occur due to unclear escalation paths or lack of preparedness. This impacts regulatory compliance and incident response effectiveness.

Lack of centralized log monitoring

Without a unified logging and monitoring system, banks struggle to detect threats in real time. The absence of centralized visibility limits their ability to correlate events and respond proactively.

Third-party vendor blind spots

Inadequate due diligence and continuous monitoring of vendors expose banks to indirect risks. Weak enforcement of security clauses and lack of audit mechanisms often lead to compliance gaps.

These gaps highlight a deeper issue: compliance is not just about implementing controls, but about continuously validating and governing them. This is where identity-centric security becomes critical. Solutions like Tech Prescient's Identity Confluence enable organizations to strengthen Identity Governance and Administration (IGA) by enforcing least privilege, automating access reviews, and maintaining audit-ready visibility across users and systems.

Not sure where your compliance gaps exist?

Use this RBI compliance checklist to identify risks, validate controls, and strengthen your audit readiness.

How Identity Governance Helps Meet RBI Requirements

Identity Governance and Administration (IGA) helps banks enforce least privilege access, automate compliance, and maintain audit-ready visibility aligned with RBI cybersecurity requirements.

Since RBI mandates strict controls around access, monitoring, and auditability, IGA solutions enable banks to enforce these requirements consistently while maintaining continuous visibility over users, systems, and data. By integrating identity with security operations, banks can move from manual compliance efforts to automated, audit-ready governance.

Here's how identity governance directly supports RBI compliance:

1. Automated Access Certification

IGA platforms automate periodic access reviews, ensuring that user permissions are regularly validated against defined roles and responsibilities. This enables banks to enforce least privilege and role-based access, implement time-bound access where required, and identify and remove dormant or excess permissions.

As a result, organizations can reduce over-permissioned accounts and maintain clear audit trails for compliance. The Reserve Bank of India framework also emphasizes controlled and time-bound system access, which IGA helps enforce efficiently.

2. Segregation of Duties (SoD) Enforcement

Identity governance solutions enforce Segregation of Duties policies by preventing conflicting access rights across critical systems. This includes implementing maker-checker style control logic where relevant, ensuring that no single user can initiate and approve the same action.

This approach minimizes the risk of fraud or misuse and ensures that no user has excessive control over sensitive operations, aligning with the Reserve Bank of India governance and risk management expectations.

3. Continuous Compliance Monitoring

While IGA platforms have evolved to offer broader visibility, their core strength lies in managing the access lifecycle, including provisioning, deprovisioning, and periodic access certifications, rather than performing real-time, high-fidelity monitoring of all user activities.

IGA helps banks maintain consistent oversight of access changes, policy violations, and entitlement ownership, ensuring that compliance evidence is always up to date. This supports regulatory expectations set by the Reserve Bank of India, while complementing SOC and other monitoring systems that handle real-time threat detection.

4. Integration with SOC & SIEM

Modern IGA platforms integrate with Security Operations Centers (SOC) and SIEM tools to provide centralized visibility and faster threat detection. By correlating identity data with security events, banks can detect anomalies, respond to incidents quickly, and strengthen overall cyber resilience. This aligns with RBI's requirement for real-time monitoring and incident response capabilities.

By embedding identity governance into their cybersecurity strategy, banks can not only meet RBI requirements but also build a more proactive, scalable, and audit-ready security framework.

Did You Know?

Over-permissioned accounts are one of the most common audit findings. Enforcing least privilege is often the fastest way to reduce risk.

Latest Updates & Future Outlook (2026)

The Reserve Bank of India Cyber Security Framework is continuously evolving to keep pace with rapid digital transformation in banking. With the rise of advanced threats, cloud adoption, and AI-driven financial services, RBI is shifting its focus toward proactive, intelligence-led security and resilience. The future of compliance is no longer static, it is adaptive, data-driven, and closely aligned with global cybersecurity standards.

1. Increasing Focus on AI-Driven Fraud

RBI has highlighted the growing use of artificial intelligence in both cyber defense and cyberattacks. Financial fraud is becoming more sophisticated, with AI-powered tools being used to detect mule accounts and suspicious transactions in real time. At the same time, RBI is working on frameworks for responsible AI adoption, ensuring that innovation is balanced with risk management and regulatory oversight.

2. Cloud Risk Management

As banks increasingly adopt cloud infrastructure, RBI is emphasizing stronger controls around cloud security and third-party dependencies. The focus is on mitigating risks such as vendor lock-in, data exposure, and lack of visibility. Financial institutions are expected to implement risk-based supervision and secure cloud configurations to maintain compliance.

3. Digital Banking Resilience

With the surge in digital payments and online banking, RBI is strengthening security requirements to ensure uninterrupted services. New guidelines such as risk-based authentication models aim to enhance fraud prevention while maintaining user experience. The central bank is also investing in platforms that can proactively identify risky transactions, reinforcing the need for continuous monitoring and rapid response.

4. Alignment with Global Frameworks (NIST CSF)

RBI's approach is increasingly aligning with global cybersecurity standards like the National Institute of Standards and Technology Cybersecurity Framework (NIST CSF). This includes adopting principles such as zero trust architecture, continuous monitoring, and identity-first security models to strengthen overall cyber resilience.

As cybersecurity threats continue to evolve, RBI's framework is expected to become more proactive, intelligence-driven, and tightly integrated with global best practices, ensuring that Indian banks remain secure, compliant, and future-ready.

Final Thoughts

The RBI Cyber Security Framework establishes a structured approach for banks to strengthen cybersecurity governance, monitoring, and incident response. Introduced through the 2016 RBI circular, it mandates board-approved policies, C-SOC monitoring, VAPT testing, and strict reporting requirements. As digital banking expands, aligning with this framework is critical for protecting financial infrastructure, reducing cyber risk, and ensuring regulatory compliance.

Tech Prescient helps financial institutions strengthen identity security, automate access governance, and address compliance gaps aligned with RBI expectations.

Want a complete, audit-ready version of this checklist?

Download a structured RBI compliance checklist to validate controls, track gaps, and prepare for audits with confidence.

FAQs

The RBI Cyber Security Framework is a mandatory directive issued by RBI in 2016 to strengthen cybersecurity across banks. It requires institutions to implement governance structures, continuous SOC monitoring, periodic VAPT, and incident reporting mechanisms. The goal is to protect banking systems, customer data, and overall financial stability.

Yes, the framework is mandatory for scheduled commercial banks as per RBI guidelines. Its principles have also been extended to other regulated entities through additional master directions. This ensures consistent cybersecurity standards across the broader financial ecosystem.

You can download the RBI Cyber Security Framework PDF from the official RBI website. Look for the cybersecurity circulars section under regulatory or notifications. The circular and related master directions are available there for reference.

The checklist includes a board-approved governance policy and defined risk management structure. It also covers SOC setup, periodic VAPT, and incident reporting mechanisms. Vendor risk management and employee awareness programs are also key requirements.

M1 to M4 represent different maturity levels defined by RBI for cybersecurity readiness. M1 focuses on basic compliance, while M2 and M3 introduce structured controls and advanced monitoring. M4 represents proactive, intelligence-driven security with higher resilience.

GET A PERSONALIZED DEMO

See Identity Confluence in Action

“One platform to govern identities, automate access decisions, and prove compliance; across every app, user, and system in your environment.”

Murli Ramsunder

Senior Architect, Vonage