On this page

See Tech Prescient in Action

Automate access, reduce risk, and stay audit-ready

The RBI Large Exposure Framework (LEF) regulates how much banks can lend to a single borrower or connected group in order to reduce concentration risk and improve financial stability. The framework aligns Indian banking regulations with Basel III standards and introduces stricter controls around large borrower exposure and interconnected lending risks.

As banking systems become more interconnected and credit concentration risks increase, the RBI continues to tighten exposure norms through updated compliance and provisioning requirements.

In this blog, we'll explain what the RBI LEF is, exposure thresholds and limits, connected counterparties, reporting requirements, and the latest 2026 RBI updates impacting banks and large borrowers.

Key Takeaways:

- The LEF caps exposure to single and group borrowers

- A “large exposure” begins at 10% of a bank's eligible capital base

- The framework applies to all scheduled commercial banks in India

- RBI's latest updates tighten rules around large borrowers and intragroup exposure

- LEF aligns Indian banking exposure norms with Basel III risk management principles

What Is the RBI Large Exposure Framework?

The RBI Large Exposure Framework (LEF) is a regulatory framework that limits how much exposure banks can have to individual borrowers or connected groups in order to reduce concentration risk and protect financial system stability.

The Large Exposure Framework RBI introduced is designed to prevent banks from becoming excessively dependent on a small number of borrowers. If a large borrower or financially connected group defaults, the impact can spread across banks and create broader systemic risk within the financial sector. The framework was introduced by the RBI in 2016 and became fully applicable from 2019 onward as part of India's alignment with global Basel III exposure norms.

Purpose of the RBI LEF

The primary objective of the RBI LEF is to reduce credit concentration risk.

Banks that lend heavily to a single borrower or corporate group become vulnerable if that entity faces financial distress. Excessive concentration can weaken bank balance sheets, increase default exposure, and create contagion risks across the banking system. The LEF helps address this by limiting how much exposure banks can maintain relative to their eligible capital base.

The framework is designed to:

- Improve credit diversification

- Strengthen banking resilience

- Reduce systemic financial risk

- Improve prudential risk management

- Align Indian banking regulations with Basel III standards

What Exposures Are Covered?

The RBI LEF applies to more than just direct loans. Banks must calculate total exposure across multiple financial instruments and commitments, including:

- Fund-based credit exposure

- Investments

- Derivatives exposure

- Guarantees and commitments

- Off-balance sheet exposure

- Counterparty credit exposure

This broader approach prevents institutions from bypassing exposure limits through indirect or structured financial arrangements.

Basel III Alignment

The framework is based on Basel III large exposure guidelines, which were introduced globally to strengthen banking sector stability after the financial crisis. Basel III emphasizes that banks should not maintain excessive exposure to a single counterparty or economically connected group because concentrated credit exposure can amplify systemic risk during periods of financial stress. By adopting the LEF, the RBI aligned Indian banking supervision with internationally accepted prudential risk management standards.

Connected Counterparty Concept

A key feature of the RBI LEF is the concept of connected counterparties. Under the framework, separate entities may be treated as a single exposure if:

- One entity controls the other

- They are financially dependent on each other

- Financial distress in one could impact the repayment ability of the other

This prevents borrowers from spreading exposure across multiple related entities to avoid regulatory limits.

Why the Framework Matters

The RBI LEF plays an important role in strengthening the overall stability of the banking system. By controlling excessive borrower concentration, the framework helps banks maintain healthier risk distribution and improve resilience during economic downturns, sectoral stress, or large corporate defaults. As lending ecosystems become more interconnected, exposure governance has become increasingly critical for both financial stability and banking risk management.

What Is Considered a Large Exposure?

Under the RBI Large Exposure Framework, a large exposure is any exposure equal to or greater than 10% of a bank's eligible capital base to a single counterparty or a group of connected counterparties. The RBI uses this threshold to identify exposures that could create significant concentration risk for a bank. Once exposure crosses the 10% limit, it falls under stricter monitoring, reporting, and regulatory oversight requirements.

The framework measures exposure relative to a bank's eligible capital base, which primarily consists of Tier 1 capital used to absorb financial losses and support banking stability.

The 10% Threshold Explained

The RBI defines a large exposure when the total exposure to a borrower or connected group reaches or exceeds 10% of the bank's eligible capital base.

For example, if a bank has an eligible capital base of ₹1,000 crore:

- Any exposure of ₹100 crore or more to a borrower qualifies as a large exposure

This threshold helps regulators identify cases where excessive lending concentration may increase systemic or operational risk.

Why does this threshold matter?

The 10% threshold acts as an early warning mechanism for concentration risk.

Large borrower exposure increases the potential impact of:

- Corporate defaults

- Sector-wide stress

- Group-level financial distress

- Contagion across interconnected entities

By monitoring large exposures closely, the RBI aims to improve banking system resilience and reduce systemic credit concentration risk.

What Counts as Exposure?

The RBI LEF considers multiple types of financial exposure, not just direct loans.

Exposure calculations include:

- Fund-based credit facilities

- Investments in debt instruments

- Counterparty credit exposure

- Derivatives exposure

- Guarantees and commitments

- Off-balance sheet exposure

This broader definition ensures banks cannot avoid exposure limits by shifting risk into indirect or structured financial arrangements.

On-Balance Sheet and Off-Balance Sheet Exposure

The framework applies to both on-balance sheet and off-balance sheet exposure. On-balance sheet exposure includes traditional banking assets such as loans and investments recorded directly on the bank's balance sheet.

Off-balance sheet exposure includes contingent liabilities and commitments such as:

- Guarantees

- Letters of credit

- Derivative contracts

- Undrawn credit facilities

Even though these exposures may not immediately appear as funded assets, they can still create substantial financial risk during periods of borrower stress or default.

Pro Tip

A borrower may appear compliant individually, but RBI LEF evaluates connected counterparties collectively. Banks must assess hidden financial dependencies, cross-guarantees, and group relationships carefully to avoid unintentionally breaching exposure limits.

RBI Large Exposure Limits Explained

Under the RBI Large Exposure Framework, banks are subject to defined exposure caps to reduce concentration risk. Exposure is generally limited to 20% for a single borrower and 25% for connected groups, with certain conditional exceptions. The large exposure framework limit is calculated as a percentage of a bank's eligible capital base. These limits help ensure that banks do not become overly dependent on a small number of borrowers or interconnected entities.

1. Single Counterparty Limit

Under RBI exposure norms, a bank's exposure to a single counterparty cannot exceed 20% of its eligible capital base under normal circumstances. In certain cases, banks may increase exposure up to 25%, but this requires explicit board approval and stronger internal risk assessment. Higher exposure levels are generally allowed only when the bank can justify the risk profile and maintain adequate governance oversight.

The single counterparty limit applies across total exposure, including:

- Loans

- Investments

- Guarantees

- Derivatives exposure

- Off-balance sheet commitments

This prevents banks from concentrating excessive financial exposure in a single borrower relationship.

2. Group Counterparty Limit

When multiple entities are classified as connected counterparties, the RBI treats them as a single exposure group. In such cases, total exposure to the group cannot exceed 25% of the bank's eligible capital base.

The RBI applies this rule because financial distress in one connected entity can quickly spread across the group through operational dependence, guarantees, ownership structures, or shared financial obligations. This group-level exposure cap is one of the most important safeguards against systemic concentration risk in corporate lending.

3. Exposure to Other Banks and NBFCs

The RBI also places exposure limits on lending and financial exposure to other banks and NBFCs. Interbank exposure limits are generally maintained within the 15–20% range, depending on the type of counterparty and exposure structure. Additional restrictions may apply for NBFCs due to interconnected financial system risks and liquidity concerns. These limits are designed to reduce contagion risk within the broader financial ecosystem, especially during periods of market stress or liquidity disruption.

Why These Limits Matter

Exposure limits are a core part of banking risk management because excessive concentration can significantly weaken a bank's financial stability during borrower distress or economic downturns.

The RBI LEF helps:

- Improve portfolio diversification

- Reduce systemic banking risk

- Strengthen prudential governance

- Prevent interconnected default exposure

- Align Indian banking practices with Basel III standards

As corporate groups and financial ecosystems become increasingly interconnected, exposure governance has become more critical for maintaining long-term banking resilience.

RBI Large Exposure Limits Table

| Exposure Type | RBI Limit |

|---|---|

| Single Counterparty | 20% of the eligible capital base |

| Single Counterparty (with board approval) | Up to 25% |

| Group Counterparty | Maximum 25% |

| Interbank Exposure | Typically 15–20% |

| NBFC Exposure | Subject to additional RBI restrictions |

Who Does the LEF Apply To?

The RBI Large Exposure Framework applies to all scheduled commercial banks operating in India, including domestic banks and foreign bank branches. The framework is designed to create consistent exposure governance standards across the banking sector and ensure that concentration risk is monitored uniformly regardless of the bank's ownership structure or operational model.

1. Indian Scheduled Commercial Banks

The LEF applies to all scheduled commercial banks regulated by the RBI, including:

- Public sector banks

- Private sector banks

- Small finance banks

- Regional operations of larger banking entities

These institutions must monitor and report exposure concentrations based on RBI-defined thresholds and capital calculations. Banks are required to evaluate exposure not only at the borrower level but also across connected counterparties and group structures.

2. Foreign Bank Branches in India

Foreign banks operating through Indian branches are also subject to the RBI Large Exposure Framework. Even if the parent entity operates globally under different regulatory frameworks, Indian branches must comply with RBI exposure norms for operations conducted within India. This ensures that cross-border banking operations maintain consistent prudential risk management practices within the Indian financial system.

Exclusions Under the Framework

Certain exposures are excluded or treated differently under the LEF framework. In general, sovereign exposures such as lending to or investments in the Government of India may receive exemptions because they are considered lower-risk from a prudential regulation perspective.

The RBI may also prescribe specific exemptions or differential treatment for:

- Central government exposures

- Certain statutory liquidity investments

- Specific regulatory arrangements

However, banks must still maintain proper reporting and classification practices for such exposures.

Why Applicability Matters

The broad applicability of the LEF ensures that concentration risk is controlled consistently across the banking ecosystem. Without standardized exposure governance, large borrower defaults or interconnected financial stress could affect multiple institutions simultaneously and create wider systemic instability. By applying the framework across domestic and foreign banking entities, the RBI strengthens sector-wide risk oversight and improves financial system resilience.

Expert Insight: The LEF's broad applicability is important because concentration risk can spread across institutions quickly when multiple banks are exposed to the same borrower groups or interconnected sectors.

Connected Counterparties Explained

Under the RBI Large Exposure Framework, entities are considered connected counterparties when financial distress in one entity could directly or indirectly impact the other's ability to repay obligations.

The concept of connected counterparties is central to the RBI LEF because banks must evaluate risk not only at the individual borrower level, but also across economically linked entities. This prevents borrowers from spreading exposure across multiple related companies to bypass regulatory exposure limits. If counterparties are classified as connected, banks must treat them as a single exposure group when calculating exposure limits.

1. Control Relationships

Entities are considered connected when one counterparty has direct or indirect control over another.

This may include:

- Parent-subsidiary structures

- Common ownership

- Shared management control

- Voting power or decision-making influence

In these cases, financial problems in one entity may quickly affect the operational or financial stability of the other entities within the group.

The RBI, therefore, treats such entities collectively for exposure calculation purposes.

2. Economic Interdependence

Even without formal ownership links, entities may still be classified as connected if they are economically dependent on one another.

For example, counterparties may be interconnected through:

- Cross guarantees

- Shared funding structures

- Significant supplier-customer dependence

- Reliance on the same revenue source

- Common financing arrangements

If the financial distress of one borrower could impair another entity's repayment capacity, the RBI may consider them connected counterparties. This prevents hidden concentration risk from building through indirectly linked entities.

3. Risk Contagion and Systemic Exposure

The connected counterparty concept is designed to reduce risk contagion within the banking system. When multiple interconnected entities fail simultaneously, banks can face concentrated losses far larger than initially anticipated. This becomes especially dangerous when several financial institutions are exposed to the same corporate group or economically dependent entities. By aggregating connected exposures, the RBI improves visibility into actual borrower concentration and systemic credit risk.

Why It Matters Under LEF

Connected counterparty classification directly affects how exposure limits are calculated under the RBI Large Exposure Framework.

For example:

- A borrower individually below the exposure limit may still trigger a breach when combined with connected entities

- Banks must continuously monitor ownership changes and financial dependencies

- Incorrect classification can lead to regulatory breaches and provisioning consequences

As corporate structures become more complex, identifying interconnected exposure risk has become increasingly important for banking supervision and credit risk management.

RBI LEF Reporting & Compliance Requirements

Under the RBI Large Exposure Framework, banks must monitor exposure limits continuously, report breaches promptly, and take corrective action within prescribed timelines. The RBI expects banks to maintain strong internal governance and risk monitoring processes to ensure compliance with LEF exposure norms. Because exposure levels can change rapidly due to lending activity, capital fluctuations, borrower restructuring, or connected counterparty classification, banks are required to track exposure concentrations on an ongoing basis.

Reporting Timelines

Banks must report any breach of RBI LEF exposure limits immediately to the regulator.

Reporting obligations apply when:

- Exposure exceeds permitted thresholds

- Connected counterparty classification changes exposure calculations

- Capital base reductions increase exposure ratios

- Temporary or exceptional breaches occur

The RBI expects banks to maintain accurate exposure reporting and provide timely disclosures for supervisory oversight.

Breach Handling and Remediation

If a bank breaches LEF limits, corrective action must typically be initiated within 30 days.

Banks may need to:

- Reduce exposure levels

- Restructure lending arrangements

- Improve collateral coverage

- Reclassify exposures

- Increase internal monitoring and provisioning

Persistent breaches or failure to remediate exposure concentration issues can result in enhanced supervisory scrutiny and additional regulatory action.

Internal Governance and Monitoring

The RBI expects banks to maintain strong internal controls around exposure governance.

This includes:

- Continuous exposure monitoring

- Board-level oversight

- Counterparty risk assessment

- Connected entity identification

- Periodic compliance reviews

Banks are also expected to maintain clear documentation and audit trails supporting exposure calculations and classification decisions.

Regulatory Oversight

The RBI uses LEF reporting as part of its broader prudential supervision and banking risk management framework.

Exposure reporting helps regulators:

- Monitor systemic concentration risk

- Identify interconnected borrower exposure

- Assess banking sector stability

- Detect emerging credit stress trends

The framework plays an important role in preventing excessive lending concentration from creating wider financial system vulnerabilities.

RBI LEF Compliance Checklist

Track exposure concentration and strengthen LEF governance controls.

RBI Large Exposure Framework 2026 Updates

The large exposure framework RBI latest updates introduce tighter restrictions on large borrowers, stricter intragroup exposure limits, and higher penalties for excessive concentration risk. The RBI's updated exposure norms are aimed at strengthening banking sector resilience and reducing systemic vulnerabilities caused by concentrated lending and interconnected financial exposures. The changes also align Indian banking supervision more closely with evolving global prudential risk management standards.

These updates are especially important for banks with significant exposure to large corporate groups, NBFCs, and interconnected financial entities.

1. Large Borrower Restrictions

One of the most significant updates under the latest RBI circular on the large exposure framework is the tighter treatment of large borrowers. For borrowers with aggregate exposure above the ₹10,000 crore threshold, banks are expected to maintain stricter exposure discipline and enhanced monitoring.

The framework also introduces the concept of NPLL (Normal Permissible Lending Limit), where incremental exposure beyond prescribed limits may be capped at 50% under certain conditions. These restrictions are intended to discourage excessive concentration in large corporate lending and reduce systemic credit dependency on a small number of entities.

2. Penalties for Excess Exposure

The RBI has also strengthened penalties for banks exceeding permitted exposure thresholds.

Where excess exposure occurs, banks may face:

- Additional provisioning requirements of up to 3%

- Increased risk weighting of up to 75% on excess exposure portions

These measures increase the capital and operational cost of concentration risk breaches and encourage banks to maintain stronger exposure governance and portfolio diversification practices. The stricter provisioning norms also improve banking sector resilience during periods of borrower stress or market volatility.

3. Intragroup Exposure Limits

The 2026 updates introduce tighter restrictions on intragroup exposure concentration.

The revised framework includes:

- Maximum 5% exposure to a single group entity

- Aggregate intragroup exposure capped at 10%

These changes are designed to reduce contagion risk within interconnected corporate structures and improve transparency around group-level financial exposure. The RBI has increasingly focused on intragroup risk because distress within one entity can quickly spread across financially connected subsidiaries, affiliates, and related organizations.

4. Foreign Bank Rule Changes

The updated framework also revises how foreign bank branches operating in India calculate and manage exposure limits. The revised exposure calculation methodology aims to improve consistency, strengthen local prudential oversight, and better account for cross-border exposure risk within multinational banking structures. Foreign banks may now face stricter local reporting, capital assessment, and exposure aggregation requirements under the revised norms.

Why the 2026 Updates Matter

The latest RBI LEF changes reflect a broader regulatory shift toward tighter concentration risk governance and more proactive banking supervision.

The updates are intended to:

- Reduce systemic lending concentration

- Improve credit discipline

- Strengthen banking resilience

- Limit interconnected borrower risk

- Enhance capital adequacy protection

As corporate groups, NBFCs, and financial ecosystems become increasingly interconnected, exposure governance is becoming a more critical part of banking risk management and financial stability oversight.

RBI LEF Before vs After 2026

| Area | Earlier Framework | 2026 Updates |

|---|---|---|

| Large Borrower Monitoring | Standard exposure limits | Stricter large borrower controls |

| Excess Exposure Penalty | Lower provisioning impact | +3% provisioning + 75% risk weight |

| Intragroup Exposure | Broader limits | 5% single entity / 10% aggregate |

| Foreign Bank Exposure Rules | Previous calculation model | Revised exposure calculation |

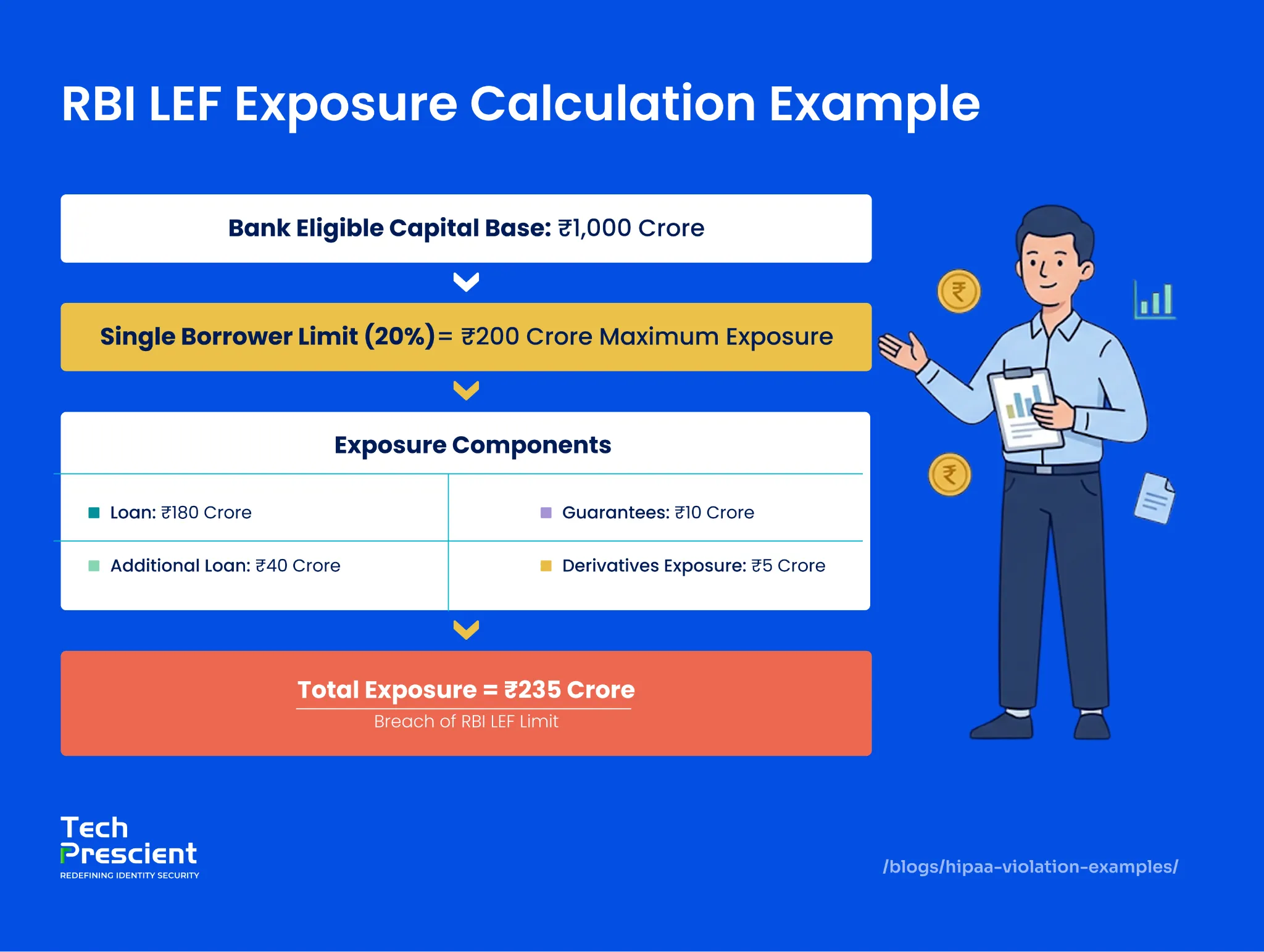

Real-World Example of LEF in Action

Under the RBI Large Exposure Framework, a bank with an eligible capital base of ₹1,000 crore can normally lend a maximum of ₹200 crore to a single borrower. A simple way to understand the RBI LEF is by looking at how exposure limits are calculated against a bank's eligible capital base.

Suppose a bank has:

- Eligible capital base: ₹1,000 crore

Under RBI exposure norms:

- A single counterparty exposure is capped at 20%

- A connected group exposure is capped at 25%

This means:

- Maximum exposure to a single borrower = ₹200 crore

- Maximum exposure to a connected group = ₹250 crore

If the bank lends beyond these limits without meeting regulatory conditions or approvals, it may trigger LEF breaches and additional compliance action.

Example Scenario

Imagine a bank has already lent ₹180 crore to a corporate borrower.

The bank then:

- Extends another ₹40 crore loan

- Provides guarantees worth ₹10 crore

- Holds ₹5 crore in exposure through derivatives

The total exposure becomes ₹235 crore.

Even though the direct loan amount alone may not appear excessive initially, the RBI LEF considers total exposure across:

- Loans

- Guarantees

- Investments

- Derivatives

- Off-balance sheet commitments

As a result, the bank exceeds the standard 20% single borrower exposure limit.

What Happens if Limits Are Breached?

If exposure breaches RBI LEF limits, the bank may face:

- Increased provisioning requirements

- Higher capital risk weighting

- Enhanced regulatory scrutiny

- Mandatory corrective action within prescribed timelines

Banks may need to reduce exposure, restructure facilities, or improve collateral and monitoring mechanisms to restore compliance. This is why continuous exposure monitoring is critical under the LEF framework.

LEF vs Earlier RBI Exposure Norms

The RBI Large Exposure Framework replaced earlier exposure norms with stricter, more transparent, and globally aligned Basel III-based risk management standards. Before the LEF was introduced, RBI exposure regulations primarily focused on traditional lending limits and borrower-level monitoring. While these norms controlled exposure to some extent, they offered limited visibility into interconnected borrower risk, indirect exposure, and systemic concentration across financial groups.

The LEF introduced a more comprehensive and risk-based framework aligned with international Basel III standards.

Earlier RBI Exposure Norms

Under earlier exposure regulations, banks primarily monitored direct lending exposure to individual borrowers and groups against simpler prudential limits.

The older framework had limitations such as:

- Less focus on interconnected counterparties

- Limited aggregation of indirect exposure

- Lower visibility into off-balance sheet exposure

- Reduced emphasis on systemic concentration risk

As corporate structures and financial ecosystems became more complex, these traditional approaches were no longer sufficient for managing large-scale interconnected exposure risk.

How the LEF Changed Exposure Governance

The RBI LEF introduced a broader and more sophisticated exposure management framework.

Unlike earlier norms, the LEF:

- Aggregates exposure across connected counterparties

- Includes off-balance sheet exposure

- Applies Basel III large exposure principles

- Strengthens exposure reporting requirements

- Improves concentration risk monitoring

The framework also introduced stricter governance around borrower interconnectedness, exposure calculation, and capital-based exposure limits.

Increased Transparency and Risk Visibility

One of the biggest improvements under the LEF is enhanced transparency.

Banks are now required to maintain better visibility into:

- Group-level borrower exposure

- Economic interdependence

- Counterparty relationships

- Aggregate concentration risk

- Exposure across multiple instruments

This improves both internal risk governance and regulatory supervision. The RBI can now monitor systemic borrower concentration more effectively across the banking sector, rather than evaluating exposures only at the individual-institution level.

Shift Toward a Risk-Based Approach

The LEF reflects a broader shift toward risk-based banking supervision.

Instead of focusing only on direct lending caps, the framework evaluates:

- Total economic exposure

- Systemic interconnectedness

- Capital adequacy impact

- Potential contagion risk

This approach aligns Indian banking regulation more closely with global prudential standards designed to strengthen financial stability after the global financial crisis.

| Area | Earlier RBI Exposure Norms | RBI LEF |

|---|---|---|

| Regulatory Basis | Traditional prudential limits | Basel III-aligned framework |

| Exposure Scope | Primarily direct lending | Total exposure, including off-balance sheet |

| Connected Counterparties | Limited focus | Central framework component |

| Risk Monitoring | Borrower-level | Group and systemic risk level |

| Transparency | Moderate | Higher exposure visibility |

| Governance Model | Static limits | Risk-based concentration governance |

Final Thoughts

The RBI Large Exposure Framework plays a critical role in reducing concentration risk and strengthening banking sector resilience. As exposure governance evolves with stricter 2026 norms, banks must improve monitoring, connected counterparty analysis, and risk management practices to maintain long-term financial stability.

RBI LEF Compliance Checklist

Track exposure concentration and strengthen LEF governance controls.

FAQs

The RBI Large Exposure Framework (LEF) is a regulatory framework that limits how much exposure banks can maintain to single borrowers or connected groups in order to reduce concentration risk and improve financial system stability.

Under RBI LEF norms, exposure to a single counterparty is generally capped at 20% of a bank's eligible capital base, while exposure to a connected group is capped at 25%. In certain cases, single borrower exposure may be extended up to 25% with board approval.

A large exposure is any exposure equal to or exceeding 10% of a bank's eligible capital base to a single borrower or connected counterparty group. This includes both on-balance sheet and off-balance sheet exposure.

The 2026 RBI LEF updates introduce stricter large borrower restrictions, higher provisioning requirements for excess exposure, tighter intragroup exposure limits, and revised exposure calculation rules for foreign banks operating in India.

The LEF applies to all scheduled commercial banks regulated by the RBI, including public sector banks, private banks, and foreign bank branches operating in India.

Share

Rashmi Ogennavar

Content Strategist

A content strategist translating complex Tech and SaaS concepts into compelling narratives for business and technical audiences. With a strategic, data-informed approach, the work bridges content and product storytelling, crafting messaging that resonates and drives decisions across the buyer journey.

Most Popular Blogs

Identity Security· 23 min read

Cyber Essentials Plus: Complete Guide to Certification, Cost & Audit

Learn Cyber Essentials Plus certification, requirements, cost, audit process & checklist. Step-by-step guide for businesses seeking compliance.

Rashmi Ogennavar· July 14, 2026

Identity Security· 22 min read

HIPAA Privacy Rule vs Security Rule: Key Differences Explained

Learn the key differences between the HIPAA Privacy Rule and Security Rule, including scope, safeguards, and how they protect PHI and ePHI.

Yatin Laygude· July 14, 2026

Identity Security· 21 min read

20 HIPAA Violation Examples (Real Cases + What to Avoid)

Explore 20 real HIPAA violation examples in healthcare and workplaces, including social media, employee access, and penalties with real cases.

Yatin Laygude· July 14, 2026